Board are funny things. They are comprised of selected individuals (directors, board members) charged with meeting together to consider various matters for the purpose of making decisions. While it is true to say directors meet, decisions are made by the collective whole—the board—not individual directors. Therefore, every decision is unanimous. Complicating matters, boards only 'exist' when directors meet, and board work is, largely, endogenous; so, they need to be coordinated—someone needs to 'drive' the board. The term 'chairman' (also, 'board chair, 'chair' or sometimes, 'chairperson') is the term used to identify the board member who carries such responsibilities—these being to convene the board’s meetings, ensure duties are discharged, and that steerage and guidance (that is, governance) is effective. But, as all directors are equal in law, the chair's role is exercised through influence, not command in any controlling sense. Given this, how should a board chair, well, chair the board? While there is no one 'best' way of chairing, the following characteristics are conducive to better outcomes:

Governance is tough because, inter alia, things change, sometimes unexpectedly; boards often need to make decisions without all the information they want; linkages between decisions and outcomes are contingent; and, directors' duties are unbounded. If boards are to govern with impact, chairs need to be alert: to ensure directors are actively engaged, and that they identify and consider relevant information, think critically and, together, make smart decisions in the best interests of the company. The chairs' priority is to convene the board and its work, and keep directors on track and the organisation safe. For this, a deft hand is needed.

4 Comments

I’ve been holidaying in Scotland this week, the first of two in the Highlands after whistle-stop visits to Edinburgh and Glasgow. I prefer the countryside over cities, the wide-open spaces and the scenery. The vistas in Scotland are especially magnificent, especially if the weather is fine, which it has been this week. Today, I saw the Jacobite Steam Train in action as it crossed the famous Glenfinnian Viaduct—well almost in action, for the chance of a wayward spark starting a fire in the adjacent bracken has limited this famous tourist experience to a push-me pull-you configuration with a heritage diesel locomotive bringing up the rear. The question, in my mind and the minds of others witnessing the viaduct crossing, was, “Which locomotive is actually doing all the work?” Or, more plainly, what is driving what? From the picture, the answer is not immediately obvious. However, the very presence of the diesel locomotive provides an important clue. And so it was. Today, the Jacobite Steam Train excursion was, in fact, the Jacobite Steam Train experience, powered by diesel. The visual imagery provides a powerful analogy for something else I saw today; a press release issued by the Institute of Directors entitled, “ESG must not neglect governance!” The headline implies that governance (from the Greek, meaning to steer, to guide, to pilot) is little more than a component of ESG (a means of measuring corporate performance). This, despite governance being the term that describes the work of the board of directors (the means by which companies are directed and controlled). But, reading on, the situation is not quite as it first seemed. Dr. Roger Barker, head of the policy unit, acknowledged the importance of boards taking non-financial (so-called, ESG) factors into account when making decisions. But he also noted the emergence of an “ESG industry” that has started to control various agendas, with little interest in the enduring performance of the company. And, with it, boards are being subordinated to a lesser role. Barker issued a strong call: to subsume governance within ESG may well result in the important work of the board in driving business performance becoming neglected. Bravo, Dr. Barker! This is exactly what institutions need to be telling their members and others interested in corporate performance: ESG is a measurement and reporting mechanism, no more and no less. The board of directors is duty-bound to ensure the performance of the company, now and into the future, a high calling. If it is to discharge its duties well, the board needs to remain in control, driving the agenda. In doing so, the board should consider various externalities including social and environmental factors), of course, but it should not be beholden to them or to those applying the pressure.

Several times in the past six weeks, I have been asked to share some thoughts on artificial intelligence and board work; specifically, the impact of emerging AI capabilities on corporate governance and, even, the need for board of directors. The rapid emergence and now widespread awareness of ChatGPT has been a catalyst for many of these enquiries, it seems. I have been fascinated by the unfolding situation, not only because of a longstanding interest (I studied artificial intelligence at university nearly four decades ago), but also the speed by which awareness has spread, and expectations climbed to such stratospheric heights, is unprecedented. Claims have been made that computer-based tools will soon supplant the need for human directors and, with it, board meetings. Some, especially those with jaundiced perceptions of boards, their work and any value they add, have confided this may be a good thing. Others have reserved judgement—for now at least—saying the situation is far too fluid and complex to make anything approaching an informed or reliable decision, much less widespread change. That so many people are questioning 'conventional' corporate governance practices feels a little bit like ground hog day. While I do not claim any particular expertise in the topic of artificial intelligence, I have read widely, asked many questions (of myself and others) and pondered both the purported capability and potential impact (of artificial intelligence) on board work. The departure points for my enquiry has been, as always, definitional. What is artificial intelligence, and what conception of governance does one hold? My responses to these questions are as follows:

So, the proposition to be considered is, "Can a computer replace a social group charged with steering and guidance an organisation in a complex and dynamic environment?" Those people wondering whether AI might be a viable mechanism to support or even replace boards have much to ponder. What is the role of a board of directors in companies? How might the operating context beyond the organisation be assessed? Where does accountability for statutory compliance and overall performance lie? And, to whom should the Chief Executive and management of the company report? If one holds the view that the board is the ultimate decision-making authority within a company (a responsibility delegated by shareholders), and that this (decision-making despite uncertainty and ambiguity) is 'core business', the board has a vital role to play. My early training in computers and technology taught me that computers respond to instruction; they cannot 'think' autonomously or handle ambiguity, and they lack feelings and intuition. They do what they are 'told'; if the 'telling' is poor, the result is likely to be poor: the phrase "garbage in, garbage out" springs to mind. But that was then. Computing power is far greater today than it was even five years ago, much less forty. Has the evolutionary development of computing capability reached the point whereby computers can displace humans? For a large and growing list of tasks and activities, yes, of course. The analysis of data is a relevant case in point. But for many other enquiries, the answers remains a resounding no. How might a computer make sense of the unspoken feelings, intuition and biases of staff, customers and board directors, and reach a credible decision? For this, a much higher order of capability is necessary. And, with that, I stand with those reserving judgement. What of the future? AI may become a viable mechanism to expedite board decision-making, of course. But the likelihood of directors being supplanted any time soon is low (those failing in their duties excepted). For that, artificial general intelligence (AGI) is likely to be necessary, and some moral and ethical questions will need to be resolved as well. If that is achieved, I may take a stronger position. Regardless of whether this muse is sound or not, directors, shareholders, regulators and their various advisors need to be alert, because the situation may change quite quickly.

The claim, that a picture is worth a thousand words, is widely known. Pictures are valuable because they capture one's attention, often evoking memories of significant or special events (as real of imaginary as they may be), or of possibilities. Indeed, the phrases 'every picture tells a story' and 'the picture tells the story' encapsulate the essence of pictures—they tell stories. But visual images are not the only means of stimulation and sharing ideas. Words are important too, especially when the ideas they convey are presented as a story. Over the seasonal break, I have been delving into a selection of books, in search of stories and ideas. The very practice of reading is, I find, a powerful enabler—to provoke, gain insight, form opinions, and learn and build knowledge about all manner of things. I have also gone back through the Musings archives and re-read many older posts. Several that piqued my attention were re-posted on LinkedIn (check my feed) to share with a new generation of readers. To my great surprise, many of these re-posts garnered considerable attention and engagement. That some ideas continue to be relevant is gratifying. Thank you to readers who have engaged with those posts. Notice the mechanism at play: hearts and minds are captured through 'story'. Pictures and words are important without doubt, but they are, simply, delivery channels: two of four mechanisms (the others being aural and kinesthetic (experiential)—together, VARK) to communicate the message. Information and its effective delivery is crucial in organisations too; board work in particular. In such situations, stories can be incredibly influential for informed decision-making, a precursor of all that follows:

As managers and directors, the way we present and consume written reports, and ask and answers questions, is material to informed decision-making. Ultimately, the board's provision of effective steerage and guidance to achieve the organisation's strategic goals depends on it. Such is the craft of board work. With this in mind, what refinements might you consider to lift your game in 2023, and lift the effectiveness of your board?

The passing of the Covid pandemic has been a great relief for many; boards of directors are no exception. Several weeks ago, I visited Sydney, Australia to meet with directors, boards and leaders of membership bodies. The feedback was clear: if companies (and through them, economies and societies) are to prosper, boards need to start thinking strategically again. Last week, more grist to the mill. During a successful visit to Bengaluru, India to lead a Board Immersion Programme for a globally-known FMCG company, the question of how boards can add value was front-of-mind throughout. Today, I'm delighted to announce my first post-Covid visit to the United Kingdom and Europe, to continue the advisory work there. From November 16th through 25th, I will visit the UK, several EU countries, and elsewhere as required, to respond to requests to speak, and to help boards respond well as they pursue sustainable business performance. This includes:

Do you want to meet in November? Regardless of whether you have a specific request or a general question, please get in touch. I'll respond promptly with some suggestions for your consideration.

I’ve spent quite a bit of time in recent weeks thinking about problem solving; my attention drawn, in particular, to problems that fall between simple (for which answers are self-evident) and wicked (easily defined, but for which an answer is elusive due to incomplete or contradictory information, or changing requirements). Difficult problems are those that can be solved, but answers are far from evident, even following careful enquiry. The BBC Series, The Bomb, explores a case in point. Nuclear fission was discovered to be theoretically possible (Leo Szilard), but considerable effort over the following decade was required to finally tackle the problem in practice. So-called ‘difficult problems’ require, clearly, intentional enquiry and, often, patience. As with gravity and magnetism, the underlying explanation (resolution) cannot be observed directly, only through its effects. So, deep and critical thinking is needed, if a resolution is to be discovered. Such problems are familiar territory for boards: if they were straightforward, management teams would resolve them. And therein lies the challenge for directors: the underlying cause of a problem raised to board level tends to be hidden under that which can be seen. And what is more, any linkage between the problem, the underlying cause, what can be observed, and any subsequent effects or impacts (note: plural) is tenuous and, almost certainly, contingent. If boards are to be effective in their work (governance: the means by which companies are directed and controlled), directors need to be alert, astute and actively engaged—more so because resolutions to difficult problems cannot be discerned directly. Thus, directors need to think beyond what is written in board reports, and what is apparent when reading other materials. Those who think they can get away with quickly reading board papers a few days before the upcoming meeting are kidding themselves. If directors are prepared to read widely across a range of topics, allocating 1–2 hours per day for six days every week, to consider ideas and think deeply, the likelihood of uncovering possibilities and solution options is greatly enhanced. Indeed, the correlation between, on one hand, time spent reading and thinking deeply, and on the other, high quality decisions is stark. Time and critical thinking matters, if directors are to add value.

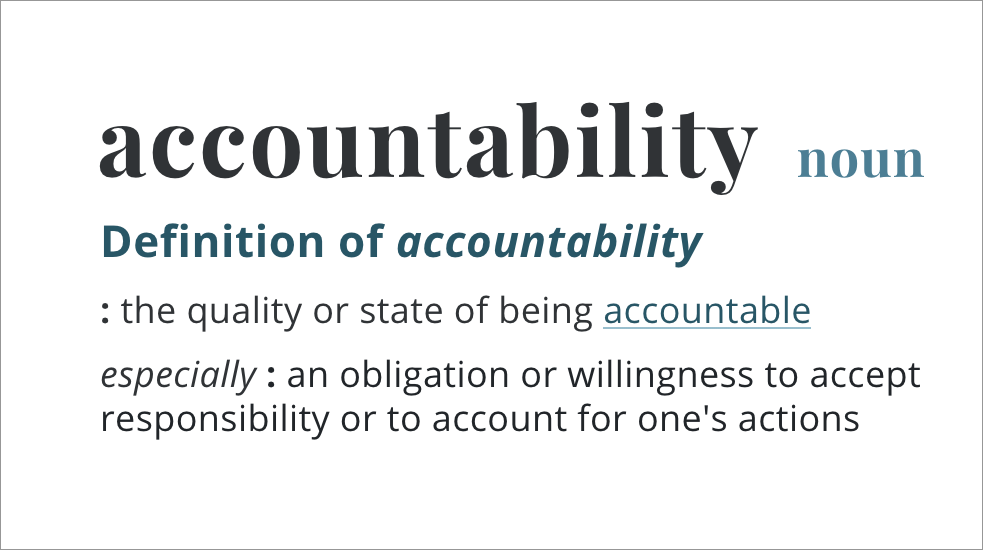

During June, I spent most of my discretionary time reviewing articles about corporate scandals and failures, as reported in the mainstream media and academic press, and discussed on social media. They made fascinating reading, not only for the summaries, but also the amount of finger-pointing and defensiveness—an indication that accountability was missing in action in most cases. Consider the Carillion, Wirecard and Petrobas cases, all mentioned in a recent Financial Times feature article (paywall, sorry). The discussion concentrated on the accounting and audit professions; the questions being whether they should have detected the problems, and whether ethics should be a consideration. These are good questions, but they sound a little like positioning an ambulance at the bottom of the cliff. Disclosures, in the form of annual reports, audit statements, and various ESG-related reports, are necessary. But they are just that; disclosure reports. And the more complex the reporting and disclosure requirements, the more time management and the board needs to spend preparing and checking reports, to meet expectations. And with greater focus on reporting and compliance, the greater the likelihood that accountability will become discretionary. Accountability is one of four foundational elements of corporate governance. There are two aspects, namely, boards are charged with holding management to account, and they need to provide an account to legitimate stakeholders. (The others are the formulation and approval of corporate purpose and strategy; policymaking; and, monitoring and supervising management, to ensure the company is operated and strategy achieved within prevailing statutory and regulatory boundaries. Together, these four elements comprise the Learning Board Framework, a proposal described in The fish rots from the head, a book written by Bob Garratt, a doyen of corporate governance and board work, circa 1996. The LBF is the single-best approach to board activity that I have come across in my twenty-five years of board and governance practice and research, bar none.) As in life, enduring success in business (meaning, achieving and sustaining high levels of organisational performance) can be attributed to many things. These include, inter alia, a great idea, a clear and coherent strategy, excellent execution, capable and highly-motivated people, forces of nature, timing, effective leadership, luck (yes, luck), and more besides. Yes, success has many sources, even to the point of being idiosyncratic. Failure is different. Even a cursory study of corporate failures reveals several common themes, most of which can be readily traced back to the boardroom:

Almost all of these themes emerge from poor behaviour and a leakage of accountability. Knowing what to do is one thing, knowing how to behave (and behaving) is quite another. Fortunately, help is at hand. Insights from research suggest five underlying behaviours are necessary if boards are to contribute well. These include strategic competence, a sense of purpose, active engagement, collective efficacy and constructive control. If any one of these is absent, the likelihood of the board exerting any meaningful influence or adding any value drops to nought. (If you want more information on this, please get in touch.) One final comment: The role of director is founded on trust—the fiduciary responsibility. And from this flows accountability—in role and in relationship. If boards place a low value on accountability, by not holding management to account for the achievement of operational and strategic goals; rubber-stamping advice from suppliers such as lawyers, accountants and auditors; or, not providing a candid account of performance to shareholders, regulators and other stakeholders, they deserve what comes their way.

The transition to electric vehicles looms large for many. Most of the major manufacturers are scrambling to offer new and exciting models to entice both corporate and private buyers. Enticements are being offered by some governments to encourage adoption. Regulators are active too, especially in Europe and California, with announced intentions to ban new vehicles powered by petrol or diesel. The opportunity to embrace a transport technology that is cleaner, quieter and considerably cheaper to operate (than petrol or diesel alternatives) is attractive—once the initial purchase price hurdle leapt. The purported benefits seem to be significant, but does the reality match the rhetoric? As with any proposal to embrace system-level change, the costs of moving from one technology to another are far from trivial. If an assessment is to be complete, the total lifetime costs (TLCs) need to be considered; that is, the sum total of all costs incurred over a product/system’s lifetime (includes manufacture, operation, disposal). In the case of electric vehicles, what of the economic, environmental and social costs of extracting metals for battery ingredients; logistics and manufacturing; replacement of batteries when they are spent; battery disposal; and, of upgrading the power generation and distribution network to provide adequate electrical power to recharge batteries? Many of these are being quietly ignored, it seems. Not my problem, some argue, as if out of sight is out of mind. This short article argues that when the TLCs are factored in, the benefits associated with a seemingly compelling technology (in this case the adoption of electric powered vehicles and other devices with battery power packs) may not be as great as what has been claimed. And so to the purpose of this muse, which is not to argue the benefits or otherwise of adopting electrically powered vehicles. Rather, it is to table an issue often overlooked by board of directors considering so-called strategic projects: total lifetime costs. When faced with a strategically-significant proposal, boards first need to check for alignment, by testing whether the proposal is contributory to the corporate strategy (spoiler alert: often linkages are tenuous). Assuming it is, directors should satisfy themselves that total lifetime costs have been included. Only then can the question of whether the recommendation should be embraced or rejected be debated. Why might this be important? Directors are duty-bound to act in the best interests of the company. That means taking all relevant information into account. If boards ignore externalities, or abuse the social, environmental and economic capitals consumed in the operation of the company, the governed company is unlikely to endure over the longer term. And in so doing, directors may be exposing themselves, unwittingly, to legal challenge as well.

ESG and sustainability are hot topics in business and, increasingly, civil society. Hardly a day goes by without one or both being mentioned in newsfeeds and across social and mainstream media. Since the term ESG was first coined in 2005, and more so through the coronavirus pandemic, researchers and commentators have promoted ESG as the answer to what have been held up as great issues of our time—issues such as changing climatic conditions; the impacts of fossil fuels; population growth; modern slavery; the excesses of capitalism; geopolitics; and, more besides. Shareholders are starting to acknowledge companies should be doing a better job, in terms of appropriately stewarding the resources used in the operation of their business and fulfilling their duties. Institutional investors in particular are applying direct pressure to refocus board attention and business priorities to tackle the great issues—their underlying belief is that ESG-based approaches provide more sustainable long-term value creation. What is one to make of these developments? Evidence to support claims that ESG-based investments outperform other investments is yet to emerge. The question of why this might be the case remains open. It could be that investments have been poorly placed; expectations are unreasonable; measurement systems are inappropriate; and, probably, more besides. Of these possibilities, the spectre of inappropriate measurement systems looms large. A couple of years ago, Ethical Boardroom, a magazine read by tens of thousands of board directors, advisors and executives, commissioned an article on the matter. I concluded that a measurement and reporting framework founded on the three main capitals used in business would probably provide a more informative and complete measure of sustainable business performance than ESG. A copy of that article follows. If you have any comments and suggestions on this, including criticisms, please do let me know—either in the comment box below or, if you prefer, a private message.

This entry is a little more personal than most posted here. But, if you'll allow the indulgence... Yesterday started out like many others before it: a mix of client and administration work, video calls across timezones, director commitments and writing (The craft of board work is coming along nicely). I 'logged off' a little later than usual—around midnight—having just completed a two-hour video call with members of the Global Peter Drucker Society (advance planning for the 2022 edition of the Global Peter Drucker Forum to be held in Vienna late this year). Tired but satisfied after a long day, I prepared for bed. And as I did, my mind wandered. March 24th was significant for some reason. Then I remembered; it was Musings' birthday! Yes, ten years ago, on 24 March 2012, I stepped, with some trepidation, into the blogosphere. That first step? A three-line post. My motivation was straightforward, to share thoughts and test ideas on corporate governance, strategy and board effectiveness. At the time, I had just started on my doctoral journey (a milestone achieved in 2016). A platform to engage with academics and global leaders—and to let off steam from time to time—was going to be helpful, I thought. And so it was, and continues to be. Today, some 712 posts later, Musings has entered middle-age. From tentative first steps, to now a library of comments on professional (corporate governance, strategy, and the craft of board work), philosophical and personal topics. Whether the thinking underpinning the articles has improved over time or not is for readers to determine. Hopefully, a progression is evident. And, while the frequency with which posts have appeared has declined a little in recent years, my desire remains as it was in 2012: that each post proved valuable to at least one person. If that was achieved, the effort was worthwhile. Looking back over the decade, I have been most fortunate to have met and learned from many great thinkers, leaders and doyens of corporate governance and strategy. I have also had the privilege of serving aspiring and established directors, and boards, across five continents. Musings has been an enabler. The support and encouragement shown as I have pursued my passion—to help boards realise the potential of the organisations they govern—has made a great difference to me. Hopefully, it has been beneficial to others as well. Thank you. And, in case you are wondering, Musings, will continue to be published, for as long as readers show interest.

|

SearchMusingsThoughts on corporate governance, strategy and boardcraft; our place in the world; and other topics that catch my attention.

Categories

All

Archives

May 2024

|

||

|

Dr. Peter Crow, CMInstD

|

© Copyright 2001-2024 | Terms of use & privacy

|